The small and medium enterprises (SMEs) make the Malaysian economy. According to the World Bank, 97% of business establishments in Malaysia are made up of SMEs. These businesses contributed nearly 36% of the country’s GDP, 65% of the country’s employment, and nearly 18% of Malaysia’s exports.

When Securities Commission chairman Tan Sri Ranjit Ajit Singh said that Malaysian SMEs are facing a financing gap of RM80 billion, this could potentially pose a problem to the country’s economic growth.

In the current landscape, SMEs have to apply for business loans from financial institutions such as banks to get a working capital injection into their business. In order to secure a loan, these SMEs are required to submit almost flawless business track record or even pledge some form of collateral before their loan application is approved. This means many of the SMEs will not make the cut.

This creates a gap that peer-to-peer (P2P) financing is expected to fill, to provide a much needed platform for SMEs to gain funding, and eventually to spur the growth of the SMEs in the country.

Peer-to-peer financing is not new globally, but Malaysia is the first country in ASEAN to regulate it. In 2014, the global P2P financing recorded a US$9 billion growth and in the following year, the number increased to US$64 billion!

Based on the global trend, does this mean an investment opportunity for investors who are looking to further diversify their investment portfolio?

How does P2P financing work?

P2P financing is also known as “marketplace lending”, where businesses can borrow money from P2P platforms like Fundaztic. Once their application is approved, the platform would assign a risk category or credit grade. The loan is then funded by individuals or a group of investors who act as the lender.

Currently, P2P financing is regulated by Securities Commission with six licensed operators in Malaysia, namely Peoplender, B2B FinPAL, Ethis Kapital, FundedByMe Malaysia, Managepay Services, and Funding Societies Malaysia.

Fundaztic, P2P financing platform owned and managed by Peoplender, offers a straightforward and transparent investment and application process for borrowers and lenders. SMEs are able to raise funds for business related purposes ranging from RM20,000 – RM200,000 and investors can invest with as little as RM50.

Why should you invest in P2P?

Investors expect to make money from their investment portfolio most years. However, in the past five years, Kuala Lumpur Composite Index (KLCI) has not been growing as quickly as investors like to see.

In 2016, KLCI was down 3%, while the MSCI Asia ex Japan index was up 3%. It has only managed to inch up 10% over the past five years, a weak performance compared to MSCI Asia ex Japan’s 16%.

In the early 2016, Jack Bogle, founder of Vanguard Funds, warned Morningstar that stock market investors were likely to see gross annual returns of just 6% over the next decade. After accounting for inflation, the real return would be closer to 4% annually.

That’s just slightly better than putting your money in a fixed deposit account. So, how can investors rebalance their investment portfolio to ensure it is performing at its peak in today’s investment climate?

With its surging popularity, P2P investing is seen as an investment vehicle that could possibly provide stable cash flow and higher returns. Depending on your investment objectives, P2P investing could have a place in your portfolio.

Here are a few reasons why P2P investing should be included in your portfolio:

1) Low entry cost at just RM50

Starting your P2P investment is easy. You can register on Fundaztic online, by providing some personal details and uploading a copy of your identity card. Once your account is verified, you can immediately start investing.

As an individual investor, you can start investing with a minimum of RM50, and are encouraged to invest not more than RM50,000. Making the minimum investment low, it gives investors the freedom to try out the platform and also the investment vehicle without taking on huge risks.

2) Potentially higher returns

The usual suspects found in an investor’s portfolio are unit trust funds, bonds and stocks. However, with KLCI giving lacklustre performance in recent years, it’s time for investors to explore expanding their portfolio to include fixed money investment that could potentially provide higher returns.

Here’s how it can potentially bring you higher return if you invest RM30,000 for 2 years in the following investment vehicles:

P2P Investing^

Fixed Deposit

Unit Trust*

Average rate of return

7.85% p.a.

4.50% p.a.

5.79% p.a.

Total returns

RM4,710.00

RM2,760.75

RM3,574.57

^ Based on Investment Note ID 16 with B3 grade. * Based on the one-year bid-to-bid annualised returns for Affin Hwang Select Bond Fund.

The above example shows gross returns, and have not taken into account the investment costs involved.

The returns will be automatically credited into your Fundaztic account, which you can choose to withdraw or invest in another investment notes.

3) Lower investment fees and charges

Investment cost is an important consideration for investors because fees and charges erode one’s investment earnings. This becomes an even more important factor to consider when your portfolio performance is below par.

Here’s the investment cost for P2P investing, if you are investing RM30,000 over 24 months.

Fee Type

Rates

Description

Amount

Verification Fees

RM0.00 – RM50.00

One-time platform verification fee charged upon making the first investment.

RM0.00

Transaction fees

RM0.00 – RM3.00

Fee charged for each investment transaction that is successfully made.

Platform Management Fees

1% of monthly repayments

Fees charged by the platform for managing the health of the invested notes for the duration of the notes / financing tenure.

(RM 1,446.25 x 1%) x 24 months

= RM347.10

Withdrawal processing fees

RM0.11 – RM1.00

Transaction charges (such as IBG, FPX) if any as charged by the banks

Total costs over 24 months

RM347.10

Compare this to the cost of unit trust investment of the same amount and tenure:

Comparing the fees and charges for both types of investment over the same period shows that P2P lending is a much more affordable investment. Currently, Fundaztic is not charging any verification fees for investors.

However, as with any investment, there are risks involved and it is important for an investor to understand his/her risk profile and the investment before taking the plunge.

What are the risks involved?

Understanding your risk profile is important before you take on any investment. At Fundaztic, investors are advised to take a questionnaire to gauge his/her risk profile, which will guide them in choosing the right investment note to invest in.

For example, for an investor between 30 and 40 years old with a Bachelor’s degree-level qualification, who would like to see moderate capital growth in his/her investments, would likely have a conservative approach towards his/her investments.

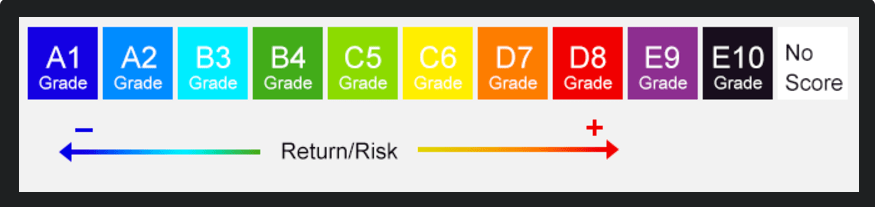

As indicated by this risk profile, the most suitable investment notes to include in the investment portfolio would be those graded A1 to B3 for funding private limited (Sdn Bhd) or partnership businesses.

Fundaztic uses the Risk Grade method to categorise “issuers” risk profile. There are 10 levels as shown in the image below. The grading is assigned based on several factors inclusive past credit behaviours as reflected in available bureau data and it will determine the amount of funds that an issuer can raise and the pricing that they must pay, among many things.

Source: Fundaztic

To help investors mitigate investment risks, Fundaztic also uses information from Credit Bureau Malaysia (CBM) report to determine the Probability of Default or PD of a business.

It is calculated using statistically valid models developed specifically for the Malaysian SME environment using various event triggers to determine how unlikely the credit will be paid in full. This will give investors an idea of the risks involved in a particular investment notes. The lower the PD, the lower the risk and the better the grade.

However, as with any investments, the higher the risk, the higher the returns. Investors should carefully analyse his/her risk profile before deciding on a particular investment note to invest in.

In short, P2P financing does have a place in your portfolio, but only if you understand how it works and the risks involved. One attraction is that you can start small with as little as RM50 plus also the significantly lower investment cost. For new investors, this is a good platform to try out as you build up your stake as you get the hang of it.

Shahril Hamdan is a man who wears many hats. But how many thirty-somethings do you know is the CEO of an oilfields company?

He joined Destini Oil in 2014 at a time when the oil and gas industry was ripe with tales of layoffs and losses.

And for the last three years, he has been hands on, putting all those experiences as a business consultant to use in tackling a battery of tests.

We caught up with Shahril to learn a little about his background, how he manages his finances and his aspirations for young Malaysians. Here’s how he spends.

Briefly tell us how you got to where you are today as CEO of an oil and gas company?

I joined Destini Oil three years ago upon its acquisition by the current parent company, Destini Berhad.

Prior to that I was working in a consulting firm, McKinsey & Company. Then, I got the opportunity to run this oil and gas services firm or drilling services firm, which was a very big jump from consulting for big multi-national corporations to actually running a local services company.

But I felt there was an opportunity for me to take the learnings I developed at my old job, to apply and see whether I was able to follow my own advice and how practical some of the consulting advice was to a real-world situation.

For someone in your position, doing what you do, share with us your money management rituals. How do you manage your finances?

Without going into too much details, I’m also involved in public life. So what I do with the salary and the income that I get, is that I tend to put them into three buckets.

The first is your personal type of expenditure: the day-to-day expenses, the groceries, and that holiday with the wife.

I am quite strict about making sure there’s always a buffer within this first bucket; so I have an idea of how much I spend every month on necessities.

I also have a second bucket which I use for my own expenses in my public life. So, if I need to travel, to do work, or if I need to fund some of the activities of a few non-governmental organisations that I run, I’ll use this bucket.

And the same process happens. I have an idea of what the mean expenditure every month is and I also know there are some months that would cost a bit more due to travel or just doing a lot more things.

So, I would plan and as I plan ahead – a month or two months ahead – to ensure that I have enough in that bucket to spend.

If there are times where bucket two is going down – I mean all these come from the same source: my salary – I will, sometimes, have to compromise or shift from one to another.

I really dislike doing that because I feel the discipline drops, but there are some times where you just have to.

So if you move, for example, from bucket one to bucket two, from the personal bucket to the work bucket, you may need to tighten belt for the next two months.

In this case, instead of going out for dinners three times a week, we go out once a week. Then you immediately see the results coming in – it’s those kind of strategies.

I also have a third bucket, where it’s for charity. Sometimes when I go to mosques and suraus, I would leave some money there. I try to do as much as I can.

Obviously it’s not the biggest bucket due to my expenses in buckets one and two, but I ensure that there is still something I can commit to every month. That’s the least I can do to give back for how lucky I have been in life.

Speaking of tracking your expenditure, do you use apps or tools?

I’m a bit of an old-school guy; I have an Excel sheet going.

I probably need to migrate at some point to an app to make it easier… but maybe this comes from my McKinsey days where Excel and PowerPoint were basically my entire life [laughs].

So, I’m very familiar and sort of versed in the mechanics of using Excel – I tend to use it quite quickly and conveniently.

But maybe I’ll try an app and see if it’s as convenient as people make it up to be. One day.

We are living in the digital age where there’s easy access to financial information. Is that a good thing?

I think this is sort of academic because you can’t control it like any other sphere of information.

Easier access to information is something we’ve got to accept as a given. The question is, is there enough financial education being given to young people especially on the different tactics and techniques to track your spending and to invest correctly and smartly.

That’s the question, right? So if there’s enough access to information about credit, there ought to be enough access to information about how you manage finances and how you think about it in the long-term.

Okay. So what’s the best way to handle credit?

Yeah, I read a stat the other day about 22,000 Malaysians under the age of 35 being declared bankrupt over the past five years. Clearly it is a problem to contend with.

I don’t know about advice but how I do it is I try to avoid personal loans, and I can share that I don’t have one, apart from credit cards.

And regarding credit cards, whatever your credit is, I don’t see that as your yardstick. I mean, banks can be quite cheeky sometimes, like all of a sudden they increase your credit to double whatever it is.

And you think, “Oh, I have more spending power.” I suppose you do, but I am quite prudent in the sense that because I track my expenses, I know how much I need to save in my first bucket.

So for my credit card expenditure, I try as far as I can to make full payment. As long as I can meet the full payment for that month, I am satisfied. This requires discipline.

Of course, there are exceptions to that, like maybe I want to get that guitar or I want to go on this holiday because I’ve worked really hard all year, then if I do any of these, I may not be able to pay the full amount, but I can clear it all within two or three months, so that the interest doesn’t hurt me so much.

I have gone as far as three months of not paying the full amount and that already got me jittery.

So that discipline of paying it off as quickly as possible… because there’s a way of racking up that credit limit and after that, you don’t change your lifestyle for the next three months and it just goes on and on, and you’ll carry a debt for the rest of your life.

Then, you’re just waiting for your bonus to pay it off, which is what I went through the first couple of years of my professional life.

I was just stuck with my credit limit and I just waited if there’s going to be a bonus on payday and then I’ll be able to pay off my credit card. Not the healthiest way of looking at things

On investments, what is your approach?

As a young person who doesn’t have a bucket of cash to be spending and investing around, I am quite balanced in my approach to it.

As a Bumiputera, I have access to Amanah Saham Bumiputera (ASB), and I’ve maxed out in terms of loans as I feel that’s a no-brainer. So that’s done, all the low-hanging fruits are done.

I withdrew some of my EPF for unit trusts. Not all of it but an amount I’m comfortable with to spread the exposures and risks because you know unit trusts are not going to be higher than your EPF returns… but they just might?

I dabble a bit in equity markets as a retail investor and I look at this the way a typical retail investor would.

So, I make some smart guesses about which counters/industries are going to show an uptrend or downtrend and I make my decisions accordingly.

Here you win some and you lose some, but for me, at this age, this may sound strange to Gen-Ys who want to make millions so quickly, but I am still at the tail end of learning these things and I want to let experience always guide me on investment decisions.

For me, it’s not about whether I win on that counter or whether I make money out of this investment in an equity market. It’s more of learning what did I misread, if I made the wrong decisions.

And hopefully, at some point, if I have more income and wealth to play with then I would have learned a lot from these experiences.

You are relatively young. Have you thought about retirement planning?

Retirement planning, sure. But retiring early, no.

And why is that?

Two reasons. First, I think it’s an unattainable goal for too many people and there’s something about Gen-Ys who do think a lot about this. There are a few examples of people who made it big, and they feel that’s something practical to aspire towards.

I don’t mean to say it’s impossible but it’s so improbable it ought to not be your guiding principle in life. Also, I doubt the people who were able to retire early set out in their early life to retire early. It’s more like, I want to do my best and if things go my way then I have that decision to make.

But you don’t work backwards. In this case, if you say you do, I think your thinking process starts getting muddle up and you start thinking of exiting early as opposed to making the right career decisions and letting things fall as they should.

The other reason is I enjoy professional life and I wouldn’t know what I’ll do if I retire early because I enjoy going to work, engaging with professionals, learning from one another and making tough decisions.

I enjoy holidays but I don’t think I would live my life as a holiday. That would be too strange for me.

Tell us the best money advice you’ve received.

It doesn’t grow on trees? [Laughs]

That it’s not everything. I’ve lived long enough to realise that there’s a point where the change in lifestyle based on money doesn’t necessarily equate better emotions or life or even utility.

And I am not a believer in this utility economics we’re taught in university anyway. I reject that notion partly because of my own experiences, in the sense that I grew up from being not-so-well-off to middle class.

I wouldn’t say I was happier then as I was when I was a kid.

Similarly, now, I’ve been lucky to experience a few salary increments, from when I first started working. You get to do different things, sure. I can go buy an expensive pair of shoes once in a while but it doesn’t give me joy.

For me, it’s about family, time you spend with people you care about. So I wouldn’t get too crazy about it.

As long as you are able to provide for your necessities, lead a fairly comfortable life or whatever you are used to, that’s enough.

In the next five years, what do you want to see changed/improved in the way young Malaysians handle their money?

I would like to see a reduction in private debt. I think young people, as we’ve discussed, have a lot to do with it. I am not blaming them but they are part of the private debt phenomenon.

Our private debt to GDP ratio is close to 90%. I think that’s something we need to be looking at more closely than, say, government debt.

There’s a lot of talk about fiscal debt and how we should address that. Actually, to me, private debt is a far more important thing to monitor.

What I hope is for young people to have enough of an income increase such that consumption is no longer driven by credit.

I think that’s where the country needs to look at very seriously, at how to increase productivity, wages and salaries. That’s your long-term solution, I think – driving growth through consumption that is not driven by credit.

So, I want that to change.

Lastly, who do you like to see answer these questions.

Nadhir Ashafiq, who runs TheLorry.com.

He made that transition from a steady income to running a start-up and I feel he has a good head on his shoulders to advice on some of these questions.

Simpan dalam SSPN-i Plus & Menangi Ganjaran Tunai Lebih dari RM500,000. Peluang besar kepada lebih 2,500 Pemenang!

Another source of good investment is invest in your child education future. Plus it covers takaful insurance and you even might win big prize!

There has been plenty of hype surrounding bitcoin and its increasing value, but is it really worth investing as much as gold is?

While saving money is important, investing it is really how we can grow our money the best way. And if you’ve been keeping up with investment news, you’ll have heard about how the cryptocurrency bitcoin have surged in value and how people have been clamouring to get in on the action. Some have even claimed that investing in bitcoinis comparable toinvesting in gold.

But how true is that? And should you start investing in bitcoin right away? Let’s find out.

Wait a Minute, Bitcoin and Gold Are Totally Different Things...

On the surface, yes. One is a shiny mineral with various industrial applications and aesthetic value, and the other is a cryptocurrency that exists digitally. However, both of these have some important similarities when looked at as investments.

Both are not tied to any government currency, which means they won’t be affected by geopolitical instability. This makes both investments attractive for people who are sceptical of traditional financial institutions or those who prefer to keep their finances separate from regular fiat currency.

Gold and bitcoin are also tremendously hard to counterfeit. Gold’s 5000-year old history of being traded as currency means we’ve developed a myriad of ways to weigh, track, and detect the purity of the metal. Bitcoin on the other hand relies on its encrypted system and complex algorithms (attributed to its blockchain technology) to ensure that no counterfeiting or fraudulent transactions with fake bitcoins could ever take place.

Another important similarity between the two is scarcity. The world’s gold supply is technically finite, and the more we dig up, the costlier it is to look for more, which in turn, will drive the price of gold even higher. Bitcoin also has a finite supply. The way bitcoin is set up, computers can mathematically “mine” for bitcoin, but there is an imposed limit to the number of bitcoins they can mine. Once this limit of 21million units is reached, there will be no more bitcoins, and where there’s a limited amount of something while demand is high, prices naturally increase to follow.

Okay, But Why is Bitcoins’ Value Getting Higher Recently?

There are several reasons for this, but without getting too technical, part of it has something to do with bitcoin’s underlying technology and efforts this year to upgrade the system to support faster, smoother transactions to help support its increasing popularity. In anticipation of this uptick in transaction volume and subsequently after the upgrade went live, prices soared.

A unit of bitcoin climbed from RM4,021 on March 16th to RM18,424 on August 16th. That’s an increase of 358%in the span of 5 months.

In comparison, gold prices per kilogram for the same period increased from RM165,756 to RM172,648. A relatively lower increase of 104%for the same 5 months.

That Sounds Great! I Should Get Some Bitcoin Right Away!

Whoa, hold on now. Just as with any hot new investment, you shouldn’t leap in head first without really knowing what you’re getting into. Especially since bitcoin is an entirely new asset class under cryptocurrency.

Since August, its value has actually dipped over some recent regulations by China. And while we’re on the subject, the legal standing of bitcoin remains a hotly discussed issue with widely differing opinions across the financial world. Countries have elected to tax it, encourage it, develop entirely new laws for it, and even ban it outright.

As far as Malaysia is concerned, while Bank Negara does not recognise it as legal tender and does not regulate bitcoin operations. This doesn’t mean you still can’t invest in it of course. It just means that if merchants offer to do business with this currency, that transaction isn’t recognised as legal. Which is tricky since bitcoin transactions are also non-reversible, so if you’ve been defrauded or scammed out of your bitcoin, there’s no getting them back.

An important thing to keep in mind is that unlike gold, bitcoin cannot function as a store of value. Since bitcoin is not linked to any government currency or any intrinsic value like gold, its price can just as easily drop to zero if enough people lose interest.

Another point against bitcoin is that it can’t yet be easily exchanged for cash. Unlike gold, which has an established history of trade and equally legal and valuable across country borders, bitcoin has different legalities and laws surrounding it and is more difficult to convert into cash in hand.

This is not to say you shouldn’t invest in it if you want to, we just want you to be aware of what you’re getting yourself into if you do. Remember: we’re a website with financial tips and stories, not an investment advice blog. All investments come with their own risks, and since bitcoin is a particularly new asset class, be careful and don’t expect too much!

Got it. So How Do I Get My Hands on Some Bitcoin?

Right now the most economical way to get some bitcoin is to buy them. There are a few ways you can do this:

Bitcoin’s decentralisation, detachment from government economy, and (near) untraceability means it’s also highly attractive for people who conduct illicit dealings. From demanding ransoms, money laundering, to the purchase of illegal goods, bitcoin has been the go-to currency.

With its current popularity as an investment asset, be aware that some people might take advantage of this and try to scam you by offering to “sell” bitcoins they don’t have. Be wary when using peer-to-peer trading services and make sure only to use trusted services.

Good as Gold?

Bitcoin is experiencing a bit of an upswing and is forecasted to continue is ascent, and it just might be a good addition to your investment portfolio. However, if you’re still on the fence about investing in it or even in gold, you can start small by setting up a fixed deposit account. It functions the same as a savings account with a higher interest rate, which makes it a good place to start. Good luck out there!